Monetary Magic or Costly Complexity? Argentina, Global Trade, and Dollarization

The U.S. dollar has become increasingly important in everyday transactions. Argentina’s new president wants to make the dollar the official currency. What can it fix and what could it break?

Argentina's Dollarization Proposal

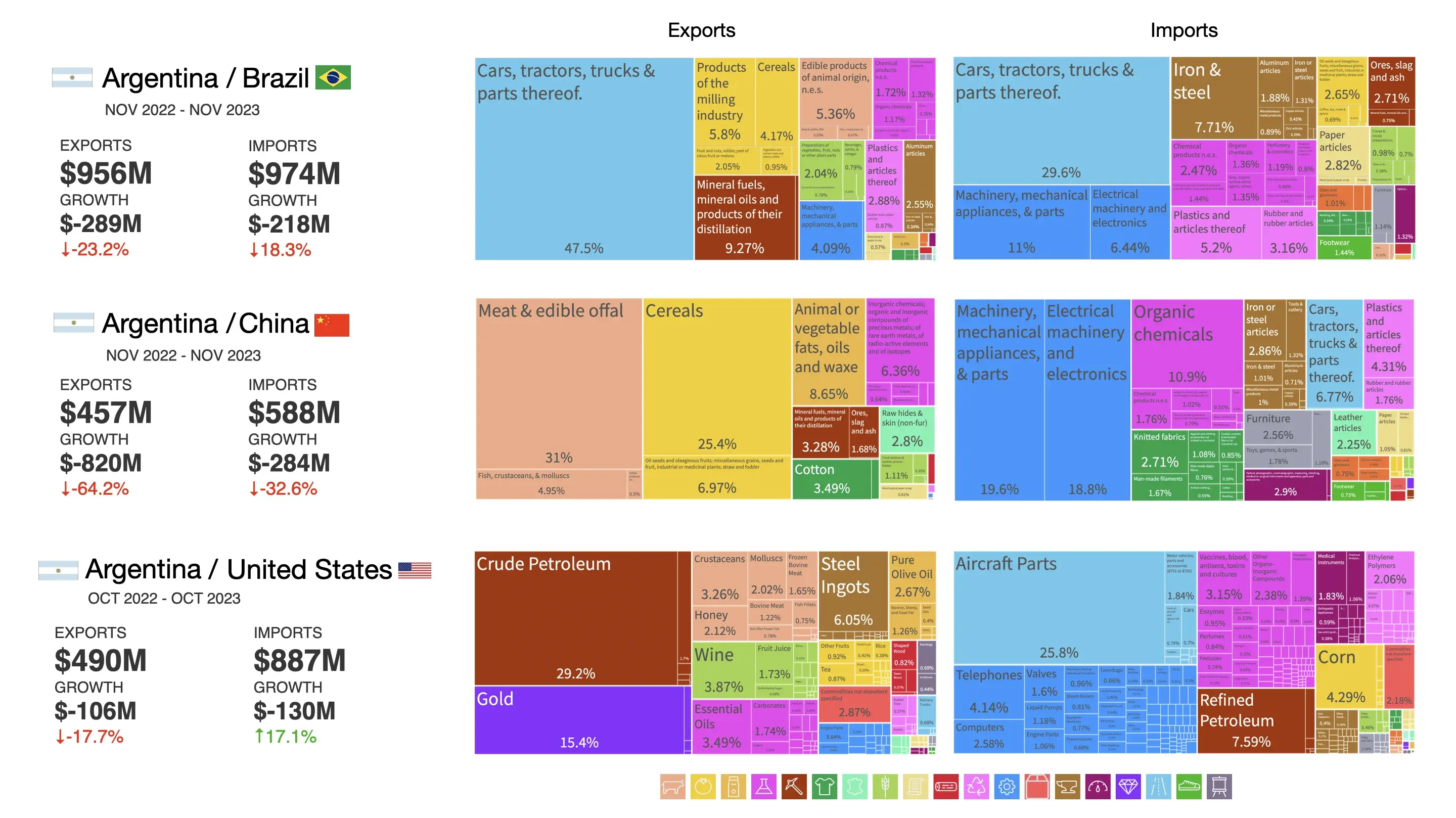

Javier Milei, President of Argentina, is considering adopting the U.S. dollar in place of the Argentine peso. Dollarization means citizens would be required to use U.S. dollars for all transactions instead of pesos. President Milei sees the dollar as a stabilizing force as a potential stabilizing force for Argentina's historically volatile economy. However, the ramifications of such a change would extend beyond Argentina’s borders, potentially influencing trade relationships with major partners such as Brazil, China, the United States, India, and Chile, which collectively account for over 50% of the country’s export destinations. These effects are complex and challenging to predict.

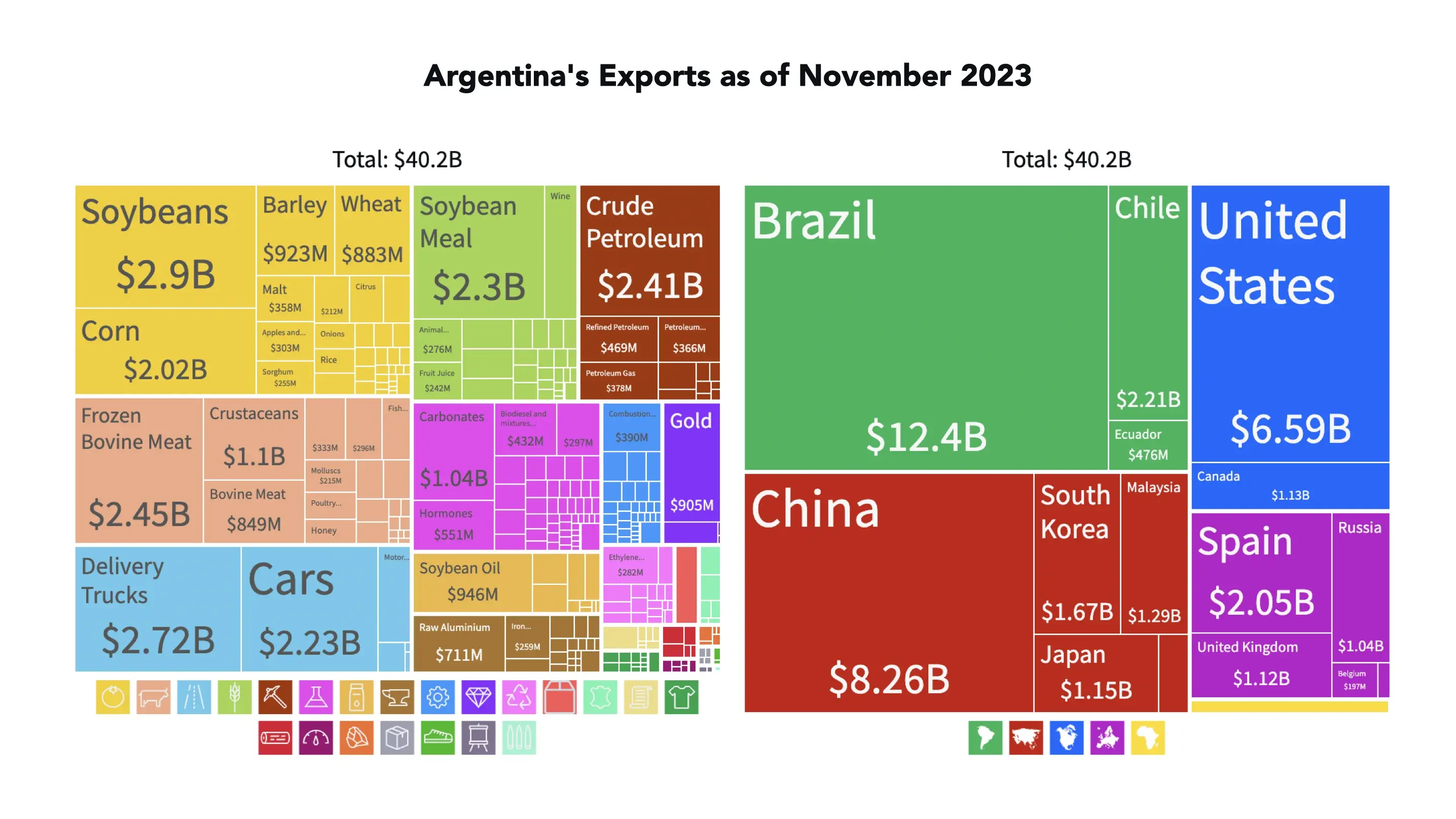

As the 28th largest exporter globally, Argentina's economy heavily relies on commodities, which comprise more than 60% of its exports. In November 2023, exports to China, including key products like frozen bovine meat and sorghum, totaled $588 million. Conversely, imports from China, primarily telephones and chemical products, were valued at $457 million. Trade with Brazil exhibited a positive balance of $17.7 million, driven by cars and semi-finished iron exports outvaluing imports of electricity and wheat. Trade with the United States was imbalanced in the other direction, leading to a significant trade deficit for Argentina.

The Exchange-Change Who Benefits?

The implementation of sudden dollarization calls for an undestanding of real exchange rate appreciation, an essential indicator for both importers and exporters. Real exchange rate appreciation reflects a currency's purchasing power in a foreign market compared to its domestic value. Argentina's adoption of the U.S. dollar may initially bring stability and boost investor confidence, potentially attracting foreign capital and increasing demand for local products and services. However, factors like aging infrastructure, high transaction costs, and existing trade barriers play a significant role in influencing the 'real' exchange rate, beyond market quotations. An inevitable rise in the real exchange rate occurs if local prices inflate or if U.S. inflation drops or maintains a lower rate. Consequently, Argentine goods and services become more expensive on the global market, despite a nominally fixed exchange rate.

The Federal Reserve focuses primarily on benefiting the U.S. economy, setting monetary policies independently of Argentina’s economic volatility, especially under dollarization. This situation leaves Argentina with limited leverage over risks to export sectors such as agriculture and mining, which are highly sensitive to price fluctuations. Sharp price increases could diminish Argentina's global competitiveness. Additionally, an unfavorable exchange rate might tip the scales in favor of imported manufactured goods, rendering them more appealing to Argentine consumers. In a dollarized economy reliant on sufficient U.S. dollar reserves, the management of foreign exchange earnings and currency-driven trade deficits becomes increasingly crucial."

Exchange Rate Rigidity: Solving a Problem or Creating One?

Adopting the U.S. dollar means losing control over currency valuation, a critical economic lever. Countries typically adjust their currency value to stimulate trade, making exports more competitive and imports more expensive. Yet, this strategy is not an option in a dollarized economy. Consequently, Argentina could experience ongoing trade deficits, particularly if its exports to China, India, or the U.S. show downturns. Moreover, Argentina's susceptibility to external economic fluctuations, such as changes in global commodity prices, could be significantly heightened, affecting dollar-reliant export sectors.

This shows how the agricultural sector, which exported significant amounts of wheat and soybeans to China, South Korea, and India in October 2023, might face reduced competitiveness and market access under dollarization. Reduced competitiveness could lead to job losses and lower wages, weakening the broader economy.

Lessons from Past Dollarizations

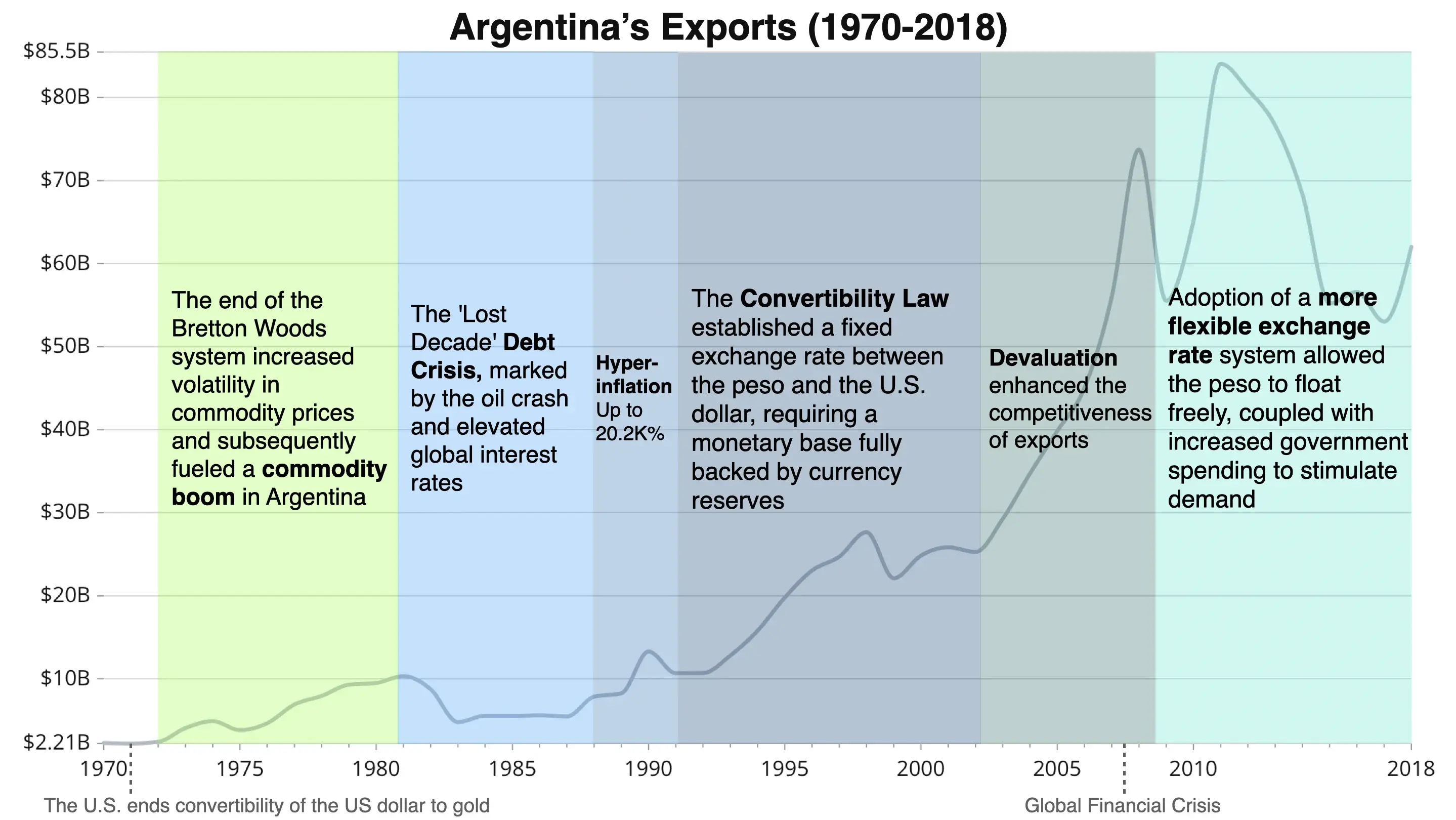

Argentina's historical flirtation with currency stabilization, specifically during the Convertibility Plan years in the 1990s, is a cautionary tale for the country’s current dollarization ambitions. The Convertibility Plan plan pegged the peso to the U.S. dollar on a one-to-one ratio, and the results produced a short-lived stability that fell apart almost immediately, leaving behind bitter lessons about the potential pitfalls of full dollarization.

Initially, the Convertibility Plan seemed a triumph, quelling hyperinflation and bringing economic stability. Yet, this was a fleeting success, soon leading to underlying systemic issues. The peg’s rigidity stripped Argentina of vital monetary policy tools, leaving it vulnerable during economic downturns and external shocks. Full dollarization would repeat that scenario unless the government enacts other safeguards to balance the effects of the loss of monetary autonomy on competitiveneess.

The Convertibility Plan made Argentine exports globally uncompetitive, leading to a ballooning trade deficit. The Plan also placed severe constraints on fiscal policy, a situation that would likely be repeated under full dollarization. The culmination of these issues was vividly illustrated in the 2001 “Corralito” crisis, a stark reminder of the dangers of rigid currency systems.

Recent experiences of other countries with dollarization also offer valuable insights:

- Ecuador (2000): After dollarization, Ecuador's inflation rate dropped from over 90% to single digits, showing immediate stabilization. However, it became more vulnerable to external shocks, such as fluctuating oil prices.

- Zimbabwe (2009): Zimbabwe's adoption of the U.S. dollar stopped hyperinflation, but it also led to liquidity problems and limited control over monetary policy, hindering economic growth.

- Panama (Since 1904): Panama has seen steady economic growth and stability with the U.S. dollar. Its unique position with the Panama Canal has significantly contributed to this success, highlighting the importance of context in dollarization outcomes.

External Vulnerabilities and Economic Dependence

As we have seen, dollarization ties Argentina's economic destiny to U.S. policies. A Federal Reserve decision to raise interest rates would tighten Argentina's monetary conditions, potentially hampering its economic growth. Fluctuations in the strength of the U.S. dollar, would be headline news in Buenos Aires, directly putting the brakes on trade competitiveness and accelerating trade imbalances.

Advocates of dollarization in Argentina recognize the challenges but believe that the benefits of stability, reduced inflation, increased foreign investment, strategic policy measures, and learning from past experiences can manage these challenges effectively. They emphasize the need for comprehensive reforms alongside dollarization to ensure its success. President Javier Milei faces balancing the short-term stability of dollarization with its broader effects on trade. He should explore alternative policies and strategies to address urgent challenges while dismantling obstacles hindering the economy.